The UK banking sector is more digital than ever, but the picture isn’t uniform. Around 1.6 million people (3% of the population) remain offline, even as cashless payments, AI-driven financial tools, and digital-only banks become part of everyday life. [1]

Reliable, up-to-date data on these shifts can be hard to find. Much of what's available lags behind the pace of real change, leaving decision-makers without the insights they need.

At Vention, we work alongside the fintechs and banks shaping this evolution firsthand. Drawing on that fintech experience, we've gathered the latest figures and trends defining banking in 2025 and beyond, with the clarity and context today's decisions demand.

How far has digital banking really come? And what gaps and opportunities are still ahead? Let’s take a closer look.

The UK financial sector at a glance

The UK has long been a global centre for international banking, insurance, bond issuance, trading, and equity capital raising. It continues to hold its position, with the financial sector contributing £197.3 billion in gross value added (GVA) to the UK economy in 2024. [46]

This contribution comes from just over 80,000 businesses operating across the finance and insurance sector, an ecosystem that combines scale with agility. However, only 235 of these companies qualify as large enterprises with 500 or more employees. [4]

A sector of this scale naturally drives employment. Today, one in every 14 UK workers, around 2.3 million people, is employed in financial and related professional services. [3]

Fintech overview

Fintech is where the UK truly shines. The country holds 11% of the global fintech market and leads Europe in fintech investment. It is home to around 2,500 fintech firms, with six of the top ten based in London. [2][3][47]

Total fintech investments by country, 2020-2024, £ billion

UK

US

Germany

France

Japan

Singapore

Hong Kong

The big picture of the UK banking landscape

When it comes to international banking, the UK leads the world. By late 2023, UK banks accounted for 14.4% of global cross-border lending, representing a staggering £4.4 trillion. [2]

Domestically, the picture is just as impressive. The Prudential Regulation Authority currently oversees around 1,300 institutions, including banks, building societies, credit unions, insurers, and major investment firms. In 2024, the banking sector employed more than 340,000 people. [5][22]

The ecosystem is broad and diverse: 42 building societies and seven credit unions in the UK, serving altogether around 26 million customers in the UK.

As for banks themselves, 362 banks were operating in the UK in 2024, a 6.8% increase on the previous year. Notably, the number of foreign banking establishments is almost twice as high as the number of UK-originated banks, reflecting the UK’s ongoing appeal as a global financial hub. [6][7][41]

UK-originated banks

EU banks

US banks

Japanese banks

Banks originated in China, Korea, and Africa

Among the UK-based banks, household names continue to dominate.

Of these, Barclays is the most popular, preferred by more than 48 million UK customers. [42]

Barclays

HSBC

Lloyds Bank Group

NatWest

Nationwide

Beyond Britain, these institutions are recognised among Europe’s financial leaders. In 2024, Barclays' market capitalisation was estimated at approximately £36 billion, Lloyds at nearly £30 billion, and HSBC stood at over £131 billion, making it the largest bank in Europe by market capitalisation. [9]

Digital vs. physical banking: Who’s leading the charge?

In 2024, 93% of UK adults used at least one form of remote banking.

Most accessed their accounts via internet portals (62%), mobile apps (60%), or telephone banking (17%). [17][48]

Percentage of people in the UK using online or remote banking, 2005-2023

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

As technology advances, customers are quick to adapt. Banking habits are changing, and physical branches are feeling the impact.

Over the past four decades, the number of banks and building societies' physical branches has plummeted by nearly 70%, from 21,643 physical offices in 1986 to 6,870 in 2024. [10]

The number of bank and building society branches, 2012-2024 [49]

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

In a letter to the Treasury Committee, Matt Hammerstein, chief executive of Barclays UK, pointed to the reasons behind this shift:

Profound technological changes, and the ease with which customers can access their accounts digitally means that our physical branch network is experiencing a sustained fall in demand.

In fact, the majority of our customers (74%) now choose to interact with us via telephone, online, or mobile banking.” [11]

Matt Hammerstein

Chief executive of Barclays UK

And the data supports this trend. More people are choosing to manage their finances via smartphone or tablet, while PCs and laptops, although in decline, still play a significant role.

Of course, technology is not the only driving factor for the shift. The COVID-19 pandemic had its say in the decline of the popularity of branch banking between 2020 and 2021. [12][13][14][15]

Let’s compare the processing methods preferred by bank account holders five years ago and in 2024

2019

2024

Yet, despite the rising popularity of remote banking solutions, 67% of Brits prefer to handle specific or complex issues on site, and more than half of the population like having a local branch nearby. [16]

Security concerns also play a role. According to LINK, about 66% of those who favour branch banking cite worries about online security, discomfort with digital tools, or greater confidence in banking face-to-face. Curiously, more than a third say they continue to use branches simply to support their local community. (Very British indeed!) [29]

Breakdown of responses when asked about current status with digital-only bank accounts

I want to support my local branch

I prefer the peace of mind of banking in branch

No real reason, I like the option of doing it in branch

I like the social interaction that comes from banking in branch

I am worried about online security

I do not trust the technology to work for online / mobile

A snapshot of Brits’ banking habits

When it comes to managing their finances, digital channels now dominate:

- A third of Brits use mobile banking daily.

- Almost a third of UK adults bank online at least once a week.

- More than a third of Brits hardly ever visit banks in branch. [18][19][20]

The takeaway is clear: convenience drives behaviour. While branch banking still has regular customers, banking in the UK has become primarily digital.

Branch banking frequency

Jul, 2019

Jul, 2020

Jul, 2021

Jul, 2022

Jul, 2023

Jul, 2024

Mobile banking frequency

Jul, 2019

Jul, 2020

Jul, 2021

Jul, 2022

Jul, 2023

Jul, 2024

Online banking frequency

Jul, 2019

Jul, 2020

Jul, 2021

jul, 2022

Jul, 2023

Jul, 2024

How digital-only banking is reshaping the traditional banking sector

Digital-only banking is no longer a niche; it is now mainstream. Since 2019, the share of UK adults with digital-only bank accounts has risen from 9% to 40% by 2025. That equates to around 21.5 million people embracing a new way of managing their finances. [21]

Percentage of Brits who have opened digital-only bank accounts

2019

2020

2021

2022

2023

2024

2025

And the momentum is still here: another 17% of UK adults will consider or intend to open a bank account with a digital-only bank in the near future. [21]

Breakdown of responses when asked about current status with digital-only bank accounts

I have opened an account with a digital-only bank

I will not consider opening an account with a digital-only bank

I am unsure whether to open a digital-only bank account

I intend to open a bank account with a digital-only bank in the future (more than a year)

I intend to open a bank account with a digital-only bank in the next year

What is driving this rapid shift, you ask? Digital-only banks often provide more attractive interest rates on savings, faster access to financial data, and simpler cross-border transactions. [21]

Reasons for choosing to open or intending to open a digital-only bank account

Better interest rates

Transfer money more easily

Using a digital-only bank is more convenient

Free transactions abroad

An easy secondary account

I think the apps are better

Friend or family recommendation

Lack of bank branches / branch closures in local areas

Neobanks vs. challengers: forging digital banking ahead

For decades, setting up a new bank in the UK was costly, time-consuming, and, more often than not, futile. Competing with the so-called Big Four (HSBC, Barclays, NatWest Group, and Lloyds Banking Group) was close to impossible.

Neobanks and challenger banks have rewritten the rules. So, what’s the difference?

- Neobanks are usually fintech companies that offer digital-only bank-like services, like payments or savings management. Neobanks do not have their own banking licence but rather partner with traditional banks to be able to provide regulated banking services to their clients.

- Challenger banks refer to smaller, recently created banks without physical branches but with an official licence. Such banks are entitled to provide a full range of banking services, which makes them strong competitors to traditional banks.

Both groups fall under the broader category of digital-only banks. Together, they have propelled the growth of the sector: by 2024, half of UK consumers had chosen a digital-only provider, up from just 16% in 2018.

However, traditional banks continue to dominate. Around 84% of primary banking relationships are still held by Britain's largest banks, while neobanks account for just 5%. [23]

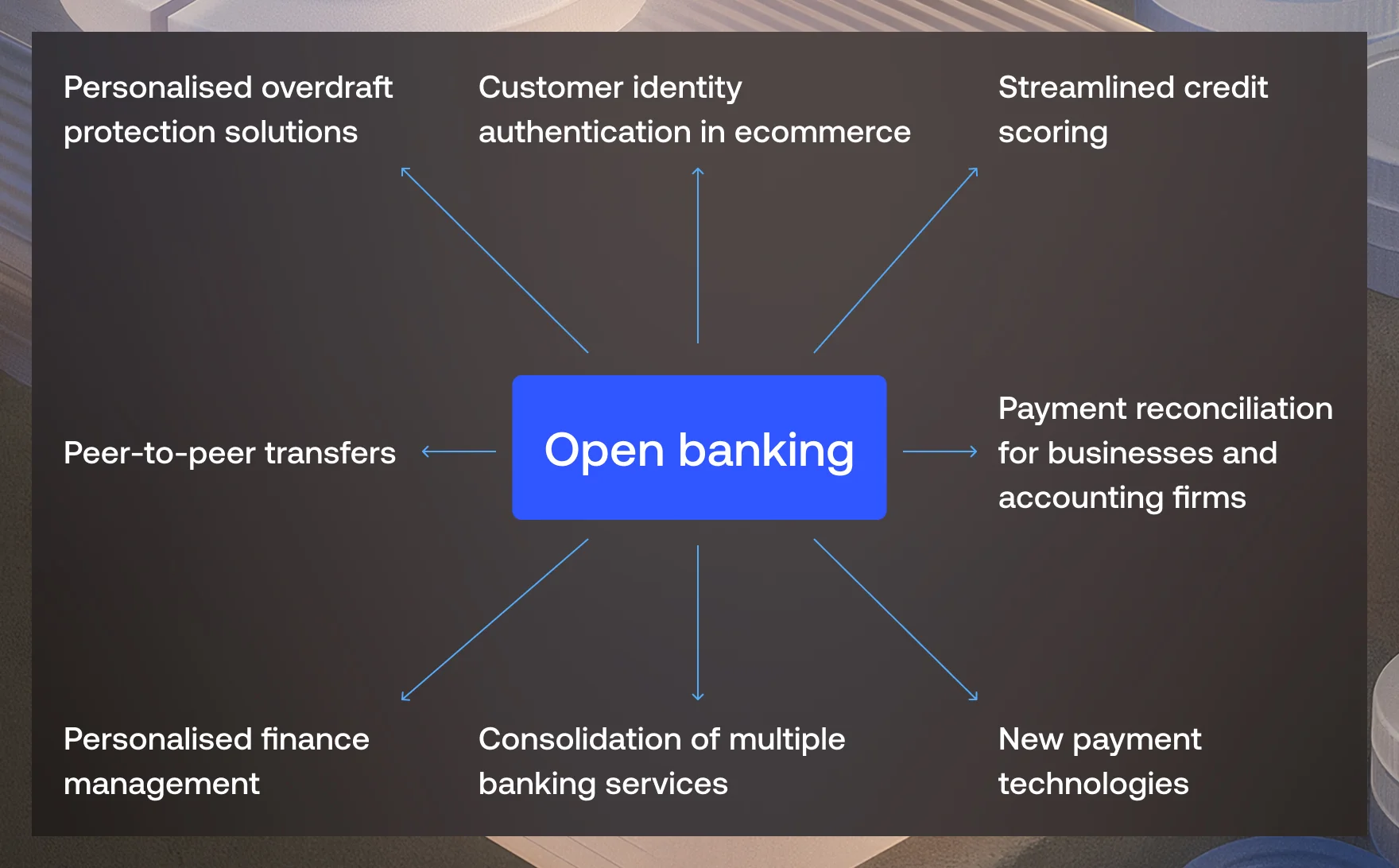

Peeling back the layers of open banking

Open banking allows for the secure sharing of customer financial data, like transaction history or balances, between banks and third-party service providers using application programming interfaces, surely with customer consent.

As of 2024, the open banking ecosystem has brought £4.1 billion to the UK economy, creating over 4,800 jobs in the sector. [24] But how did this transformation unfold?

The history of open banking in brief

Pre-2015: A call for change

Large banks dominate the UK financial sector, and the industry lacks innovation and offers limited customer choice of banking providers.

2016: Building the foundation

After extensive research, the CMA mandated that the nine largest UK banks enable customer data sharing with trusted third-party providers using secure APIs. As a result, the Open Banking Implementation Entity (OBIE) was established to oversee the development of a secure API standard and data-sharing framework.

2018: Open banking launch

The revised Payments Service Directive 2 (PSD2) comes into force across the EU along with the launch of Open Banking in the UK, which went live on 13 January 2018.

2019 - 2023: Gradual adoption

With initially slow adoption due to the lack of awareness, open banking gradually gained popularity, resulting in 6.5 million active users of open banking-enabled products in the UK, and the CMA announced the completion of the open banking implementation roadmap. [25]

2025: Full steam ahead

In 2025, nearly 12 million people in the UK actively use products powered by open banking, with more than 22.1 million open banking-enabled payments made each month. British consumers have gained a simpler, more secure way to manage their finances. [26]

How open banking is used, and why it matters

UK consumers, businesses, and fintech innovators use open banking solutions to streamline payments, improve financial control, and consolidate financial services.

Top use cases among UK consumers

Percentage of UK consumers | Benefit | |

|---|---|---|

Sending money to others | 72% | Seamless and secure account-to-account payments and transfers |

Paying bills | 66% | Streamlined financial management, and timely automated bill clearing |

Banking services | 66% | Improved user experience and satisfaction with innovative and efficient banking solutions |

What drives UK consumers to adopt open banking?

- 57% of Brits choose open banking solutions for the time savings they offer.

- 52% value the ability to make seamless and secure payments.

- 50% use open banking tools to conveniently track financial activity across multiple accounts. [27]

The future of open banking

The future looks bright for open banking in the UK. Adoption is set to keep rising, with 61% of Brits likely to use open banking services in the future. [27]

And the ideas and technology behind open banking became a foundation for the Data (Use and Access) Bill. Inspired by open banking, the Bill seeks to expand the open banking model to other sectors, such as energy, telecoms, and insurance. By enabling greater access to the sharing of smart data, the Bill aims to give consumers more control and to drive innovation across industries.

AI in UK banking: What’s hype and what’s already here

Artificial intelligence is reshaping the financial sector, and the technology is doing it fast. As of 2025, 75% of UK financial firms, including banks, insurance, investment, and non-bank lending companies, have already been using AI tools.

And another 10% are planning to expand AI usage in the next three years. This marks a significant jump from 2022, when only 58% of firms reported using AI to streamline their operations. [30]

UK-based vs. international banks in the UK: Who’s leading the AI adoption?

Looking at banks specifically, international banks operating in the UK are leading the way in AI adoption, leaving UK-native banks slightly lagging behind.

However, given the sector’s long-standing reliance on traditional workflows and, often, legacy systems, the fact that over half of UK-native banks have adopted AI is a roaring success. [30]

UK banks | International banks in the UK | |

|---|---|---|

Percentage of AI adoption | ~65% | 94% |

Planning to adopt AI | >10% | 6% |

Where AI is gaining ground

AI tools have gained significant traction in automating back and middle office operations:

- 41% of UK financial firms use AI to optimise internal processes.

- 37% for cybersecurity.

- 33% for fraud detection.

However, the reality still lags behind the hype, particularly in customer-facing applications.

Front office AI: Progress, but not yet mainstream

Despite the buzz around AI-powered chatbots and virtual assistants, front office applications remain in the early stages.

While some companies have introduced AI-enabled services, challenges around regulation, data privacy, and security persist. Experts suggest it will be at least another two years before AI becomes a reliable tool in front-line banking operations. [30][31]

Front office | Middle office | Back office | |

|---|---|---|---|

Current stage of AI adoption | Weak/Moderate | Moderate/Strong | Strong |

Examples | Sentiment analysis, customer communication script generation, AI-enabled chatbots | Automated underwriting processes, compliance and regulatory reporting, fraud detection and prevention | Streamlined IT engineering, automated code tests and mock data generation |

UK banks warm up towards blockchain, though carefully

First proposed in 2008 as a decentralised, cryptographic ledger, blockchain technology has sent shockwaves through the financial sector. Bitcoin, a blockchain-enabled cryptocurrency, became the first practical implementation of the idea and brought the potential to upend traditional banking.

But how do banks in the UK approach everything starting with “crypto”?

Historically, with caution. While some countries welcomed crypto with open arms, UK banks have taken a more conservative stance. Restrictions are common:

- HSBC has introduced limits of £2,500 for a single transaction and a total of £10,000 in any rolling 30-day period.

- Santander prohibits payments to Binance.

- Lloyds Bank bans buying cryptocurrency on its credit cards. [32][33]

And the resistance is not without reason: against the backdrop of unclear government regulations in the domain, UK banks want to protect their clients from scams and fraud.

Shifting tides: From resistance to regulation

However, the landscape is beginning to change. One real-world example is London-based fintech company Fnality.

In December 2023, Fnality launched the Sterling Fnality Payment System (£FnPS), marking the world's first fully regulated blockchain-based payment system for central bank money. £FnPS is recognised by HM Treasury as important, and operates under the oversight of the Bank of England and the UK's Payment Systems Regulator. [35]

Legislation is another step towards blockchain adoption in the UK. The UK government marked the beginning of 2025 by publishing a draft of legislation for managing crypto assets. The new Plan for Change is supposed to protect people’s assets while leaving sufficient space for innovation in the domain. [34]

Cloud adoption by UK banks

Back in 2021, 33% of UK financial firms had already implemented cloud at scale, 42% had begun adoption, and 21% were planning their move. Fast forward to 2025, and the cloud has firmly taken root among UK banks. Institutions are embracing the cloud to cut costs, boost scalability, agility, and security. [37]

Here’s how UK financial leaders are putting the cloud to work.

Starling Bank: A cloud-native challenger

A UK financial services disruptor and digital-only bank, Starling Bank has used AWS services to build and host all of its infrastructure from day one.

The cloud-first approach helps the bank avoid the capital expenditure of on-premises IT infrastructure hosting and management, enables fast and easy scaling, as well as ensures robust data security. [38]

Nationwide Building Society: Modernising payments

In a bid to transform its payment infrastructure, Nationwide, the UK’s largest building society, partnered with AWS and Form3.

The result is a new cloud-first payment platform based on API and microservices architecture. The new system offers uninterrupted, seamless service, capable of handling 500 transactions per second, or more than one million transactions per day. [39]

Atom Bank: Embracing cloud for scalability

The UK’s first app-based bank, Atom Bank hosted its infrastructure at a third-party data centre.

Following rapid business growth, Atom Bank decided to switch to the cloud alternative and completely rebuilt its infrastructure using Google Cloud tools. The shift increased application speed, reduced latency, and improved the overall customer experience [40]

Cybersecurity concerns: digitalisation in UK banking comes at a price

Digital banking does offer speed and convenience, but does not come without risks, and consumers remain cautious. As of 2025, 12% of UK adults say they won’t consider opening a digital-only bank account due to risks of payment fraud or cybersecurity breaches.

These concerns are not unfounded. In 2023, unauthorised fraud losses totalled £708.7 million, with £152 million attributed to fraud via remote banking channels. [21][36]

As mobile banking popularity significantly grows, so does the number of related fraud cases. In 2023, mobile banking fraud alone accounted for £45.5 million in losses, which is a 62% increase from the previous year. And for the first time in history, the number of mobile banking fraud cases (20,032) surpassed those related to internet banking (13,669). [36]

Efforts to prevent banking fraud

Despite the scale of the problem, government and banking authorities are working hard to fight back against remote banking fraud. In 2023, the overall remote banking fraud prevention rate reached 59%, a 25% improvement compared to 2022. [36]

2015

2016

2017

2018

2019

2020

2021

2022

2023

What’s next for banking in the UK?

The future of banking in the UK is being shaped by a blend of tech innovations, growing customer expectations and the wider macroeconomic environment.

We will continue to see increasing regulatory approval for the use of AI, just as we saw for cloud technology back in 2016. And while we’ve seen a decline in the use of cash in recent years, it would be wrong to assume we’re on the verge of becoming a fully cashless society: cash is still important for many and isn’t going away completely any time soon.”

Technical Manager at Vention

Increasing AI integration

Banks are accelerating their digital transformation, and artificial intelligence is leading the way. The market for AI in UK financial services is projected to grow from £933 million in 2023 to an estimated £8.7 billion by 2032, with a compound annual growth rate (CAGR) of 28.1%. [45]

Branch closures on the horizon

As digital banking becomes the norm, more physical branches disappear from the high street. Santander plans to shut down about 95 physical branches in the UK by the end of 2025 and focus on improving its mobile banking application, web chat, and telephone services.

At the same time, Lloyds, Halifax, and Bank of Scotland, which are all part of the Lloyds Banking Group, are expected to close at least 254 bank branches in 2025 and 2026. [43][44]

Going cashless

The use of cash has dropped significantly in recent years among UK citizens. [17]

Cash as a percentage of all payments

2008

2013

2018

2023

ATM cash withdrawals are also declining. In 2024, the total volume of cash withdrawals was roughly half what it was in 2018. [28]

Total cash withdrawal volumes (£ millions)

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

So, how close are we to a cashless society? Despite the general downward trend, the number of people using cash for their day-to-day purchases in 2023 grew to 1.5 million consumers from 0.9 million in 2022. Why? Economic uncertainty.

Having money physically in hand gives consumers more control over their spending and savings. Without the widespread availability of digital budgeting tools and mobile banking apps (particularly among younger generations), the share of cash payments would likely be even higher.

The road to 2033: Digital-first, not digital-only

By 2033, the payment landscape in the UK is expected to look very different:

- Contactless debit and credit card payment volumes will exceed 25 billion payments, accounting for 45% of all payments made in the UK.

- Faster Payments and other remote banking will grow to 7.2 billion payments.

- Cash payments account for around 6% of all payment volume, approximately 3.4 billion transactions.

The UK may not become entirely cashless in the near future, but the shift is unmistakable. Cash will continue to serve specific groups, yet it will no longer hold the central role it once had. [17]

Digital banking moves fast. Vention is here to help you innovate with confidence

Building the next generation of banking products means navigating cybersecurity threats, rising customer expectations, and complex regulatory demands, all at speed and without compromise.

With decades of experience in cloud, AI, facilitating compliance, and financial software development, we turn complexity into clarity, helping you deliver digital innovation securely, seamlessly, and with engineering peace of mind built in.

The UK-based partner you’ve been looking for

In London? Let’s talk your project over in person.

Churchill Place

London E14 5RE, UK

List of sources

Sources

- Lloyds Bank, 2024 Consumer Digital Index

- State of the sector: annual review of UK financial services 2024

- GOV.UK/Financial services sector

- Statista

- Bank of England – Which firms does the PRA regulate?

- IBISWorld

- Institutions in the UK banking sector, April 2025, Bank of England

- Financial services in the UK, House of Commons Library

- Largest banks in the United Kingdom (UK), Statista

- House of Lords Library, Closure of bank branches: Impact on rural communities

- House of Commons Treasury Committee, ‘Barclays UK reply to Treasury Committee letter concerning bank branch closures’

- Methods of processing banking affairs in the United Kingdom (UK) in 4th quarter 2024, Statista

- Share of bank account holders processing banking matters via mobile banking (smartphone or tablet) in the United Kingdom (UK) from 1st half 2019 to 4th quarter 2024, Statista

- Share of bank account holders processing banking matters via online banking (PC or laptop) in the United Kingdom (UK) from 1st half 2019 to 4th quarter 2024, Statista

- Share of bank account holders processing banking matters in person in a branch in the United Kingdom (UK) from 1st half 2019 to 4th quarter 2024, Statista

- Banking Consumer Study: Reignite human connections, Accenture

- UK Payment Markets Summary, July 2024, UK Finance

- YouGov UK, How often Brits visit their bank in branch

- YouGov UK, How often Brits use mobile banking

- YouGov UK, How often Brits bank online

- Finder UK analysis, Digital banking statistics 2025: How many Brits use online banking?

- ONS, Banks count and employees for 2023 and 2024

- RFI Global, The future of banking: Five strategies for banks and fintechs

- ‘The Future is Open’ report, Alvarez & Marsal

- Open Banking Limited, press release, 13 January 2023

- Open Banking Limited, press release, 13 January 2025

- Mastercard Open Banking, The acceleration of open banking in the UK

- LINK, How people use cash

- LINK, Is the UK ready to go digital?

- Bank of England, Artificial intelligence in UK financial services - 2024

- The reality of AI use in banking and financial services, Alvarez & Marsal

- HSBC UK, Preventing cryptocurrency fraud

- Santander Bank Support

- GOV.UK, New cryptoasset rules to drive growth and protect consumers, Press release

- Fnality

- UK Finance, Annual Fraud Report 2024

- UK Finance, Cloud Adoption 2021

- AWS Case Study, How Starling Bank is disrupting the banking industry

- Accenture Case Study, Nationwide races into the payments future

- Google Cloud Case Study, Atom bank: Empowering a digital-only bank to transform the way people handle their finances

- Building Societies Association

- Finder UK analysis, Banking statistics UK: Biggest banks by market share and customers

- MSE News, March 2025

- MSE News, January 2025

- Credence Research, UK Artificial Intelligence in Finance Market

- Statista, Gross value added of the financial and insurance services sector in the United Kingdom from 1990 to 2024

- Dealroom

- Financial Lives 2024

- Dataset: UK Business Counts - local units by industry and employment size band, accessed in June 2025