How Banking as a Service reshapes the financial services industry

The recent years have shown how traditional banks are being challenged by neobanks, fintech startups, and other players in the booming financial services market, especially in the light of the growing demand for remote services.

With the digital transformation pervading the dynamic financial services sphere, new business models and technical advancements are coming to the fore. One of them is Banking as a service (BaaS), which helps both the incumbents that strive to go digital as well as startups that drive fintech innovation to stay ahead of the game.

Established banks have been leveraging Banking as a Service to simplify their operations, migrate from legacy systems, and come up with new customer propositions rapidly. In their turn, startups value BaaS for the opportunity to reduce operational costs and get to the market with unprecedented speed.

Are you looking to make your way to the market, too? If so, then keep reading to learn about what banking as a service is, how it works, the leading BaaS providers, and key benefits.

What is Banking as a Service?

Banking as a Service (BaaS) is an end-to-end process implying that fintech startups and other companies connect to a bank's system using APIs. It's done to create new banking services and offerings on top of the provider bank's infrastructure. Thus, partnering with banks helps fintech's and non-banking organizations create their products and introduce them to the market quicker, without huge prior investment in purchasing infrastructure and building the new banking services from scratch.

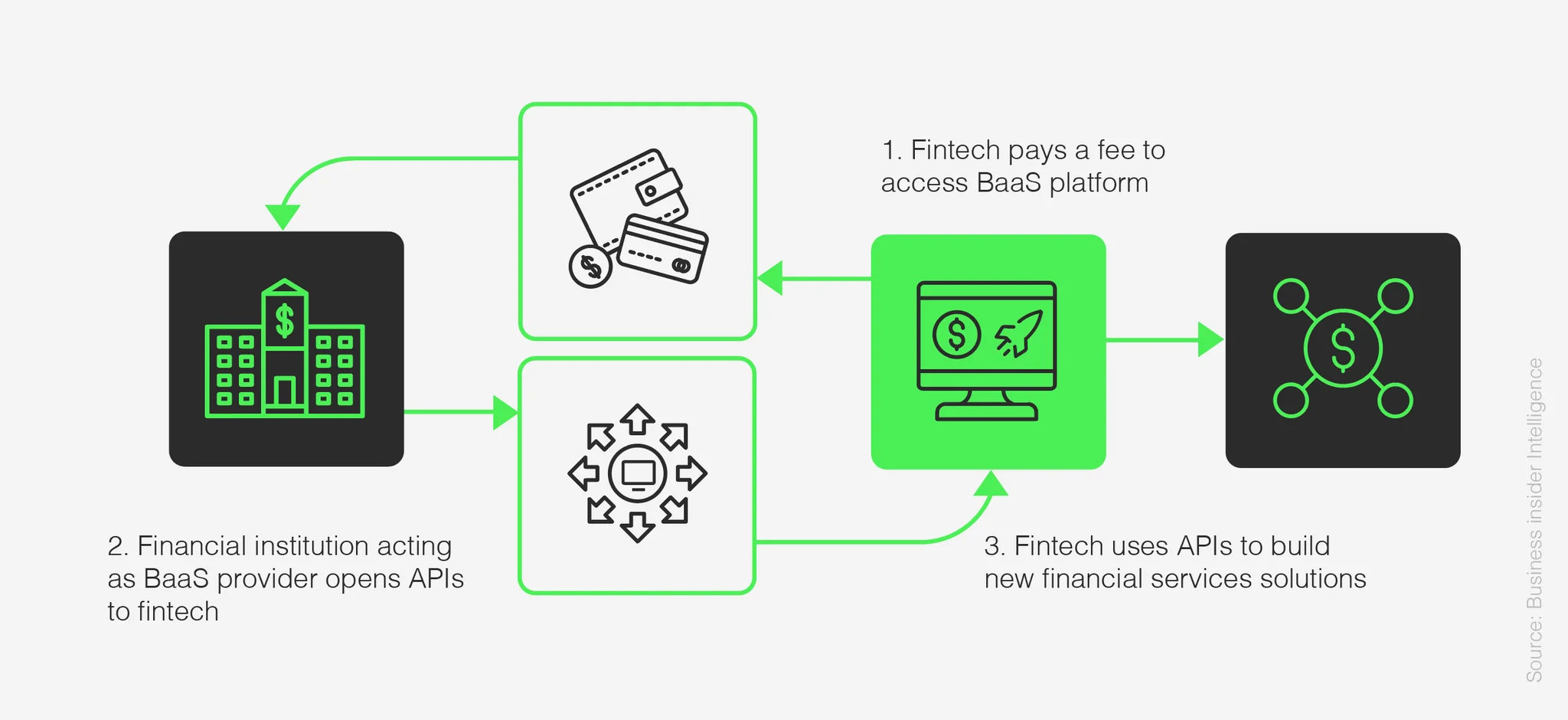

How does Banking as a Service work for fintech?

The process consists of three steps. It all starts with a fintech, or any other third-party organization purchasing the access to the BaaS platform (paying either monthly fees or paying for each service used) to create their products and features on top of the existing banking infrastructure. After that, the bank that acts as a BaaS provider grants fintech access to its APIs. Finally, fintech or another third-party services provider (TPP) leverages the bank APIs to develop new fintech products and launch new financial services, such as digital lending, payment, and account management services in their own applications.

Top Banking as a Service providers

There are two groups of BaaS providers:

1. Established banks (also called Banks with BaaS) keep up with the main financial trends and therefore partner with fintech's and third-party companies, providing them access to their banking infrastructure and systems. Among the banks that pioneer the BaaS segment are:

- Starling Bank: This British retail bank allows partner fintechs and banks to provide their customers with streamlined accounts opening, keeping, managing, and transferring funds, KYC and AML services, etc.

- BBVA: As the first bank in the United States to make BaaS products available, BBVA now supports a huge number of third-party organizations with its scalable banking infrastructure. Its platform supports card issuance, account management, customer identity verification, and other banking functions.

- ClearBank: This UK clearing bank delivers comprehensive banking services with its in-house banking infrastructure.

2. BaaS-focused fintechs (or pure BaaS providers) provide banking software as a service to other companies wishing to launch new financial products on the market quickly. The list of the top pure BaaS providers includes:

- Solarisbank: This German BaaS provider has a banking license, which means the company will be carrying a regulatory burden while its customers can leverage its comprehensive BaaS platform. It allows the building of truly innovative banking products for offering debit cards, consumer and SME loans, payment services, KYC services, and more.

- Synapse: Synapse offers a banking infrastructure to fintech companies that builds payment, deposit, lending, and investment products as APIs on top of it.

- PayPal: The online payments system enables sending or receiving payments to and from other PayPal accounts online or via the company's app.

The incomplete list of banking services covered by BaaS providers from the two aforementioned groups include:

- Account management

- Credit cards management

- Issuing and managing debit cards

- Providing consumer and SME loans

- Deposit management

- Know-your-customer (KYC) services

- Anti-money laundering (AML) services

- Product management

The benefits of BaaS

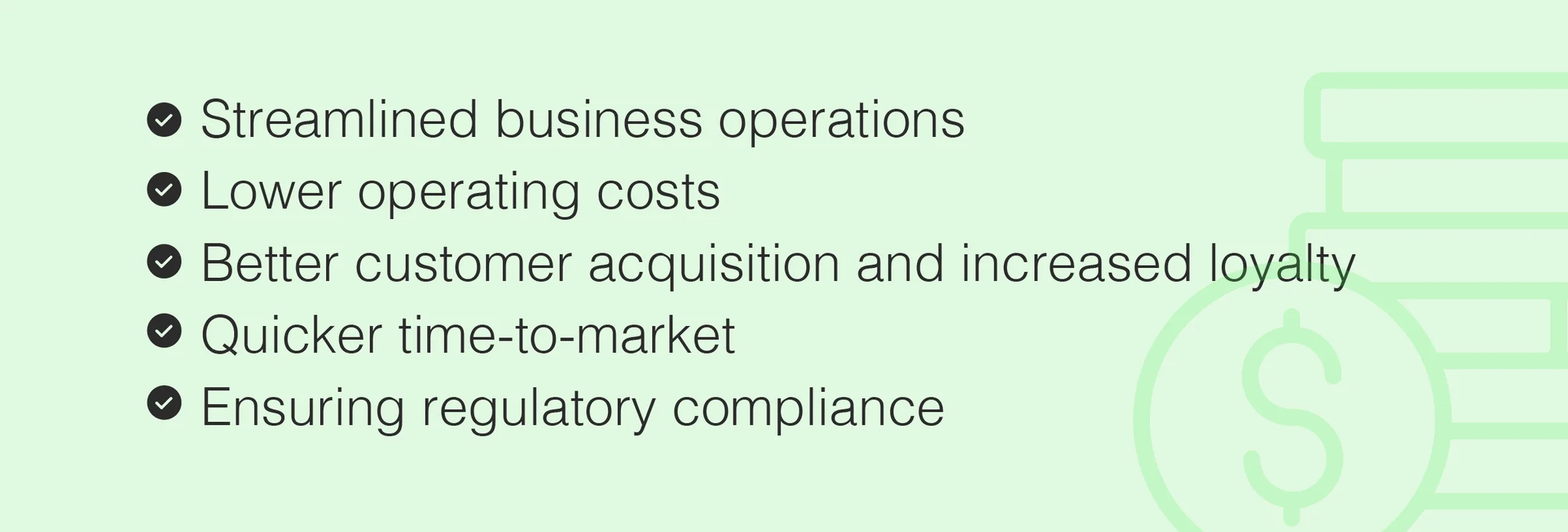

As stated in Capgemini's World Retail Banking Report, over 80% of clients that plan to switch financial services providers in the next three years use a banking product from a big tech firm or digital bank. The demand for BaaS is steadily growing, and it looks like a deal equally beneficial for both BaaS providers and their client companies. Here's how third-party companies benefit from leveraging BaaS for their business:

- Streamlined business operations due to banking services incorporated in the company's own platform/solution.

- Lower operating costs with no need to build and maintain a banking infrastructure from scratch.

- Better customer acquisition and increased loyalty due to superior customer experience.

- Quicker time-to-market as there's no need to build a banking product from the ground up, and the main development issues can be solved by accessing the BaaS platform's functionality.

- Ensuring regulatory compliance. Compliance with manifold regulations is a heavy burden for companies entering the financial services market. By partnering with banks and other BaaS providers with a banking license, third-party companies take this burden off themselves.

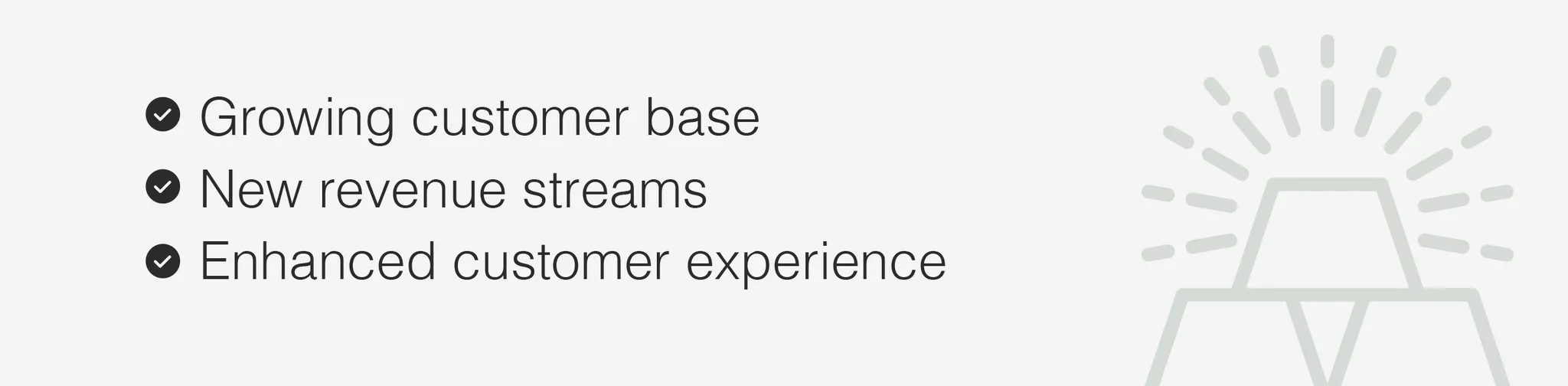

As for the BaaS providers, they get:

- Growing customer base. When banks provide BaaS services to third-party companies, they get access to huge customer bases of these companies at little cost, and they may see many of these people among their potential clients.

- New revenue streams. Creating a BaaS platform and providing fee-based access to it turns into another revenue source valued by any bank that strives for a bigger profit.

- Enhanced customer experience. By integrating the services of external companies into their own offerings made possible with BaaS, banks can create end-to-end processes that contribute to superior user experience.

Where's BaaS headed?

It's already clear that leveraging Banking as a Service has become a must for any bank or fintech startup looking to stay ahead of the competition, grow its market presence, and spearhead the digital transformation in the financial services domain. Thus, it's no surprise that the global digital banking platform market is expected to reach $8.67 billion by 2027. Though being disruptive by nature, BaaS doesn't act as a disruptor. Rather, it reinforces the financial services market, making it more innovative and customer-centric, and paving the way to effective collaboration of the market players.