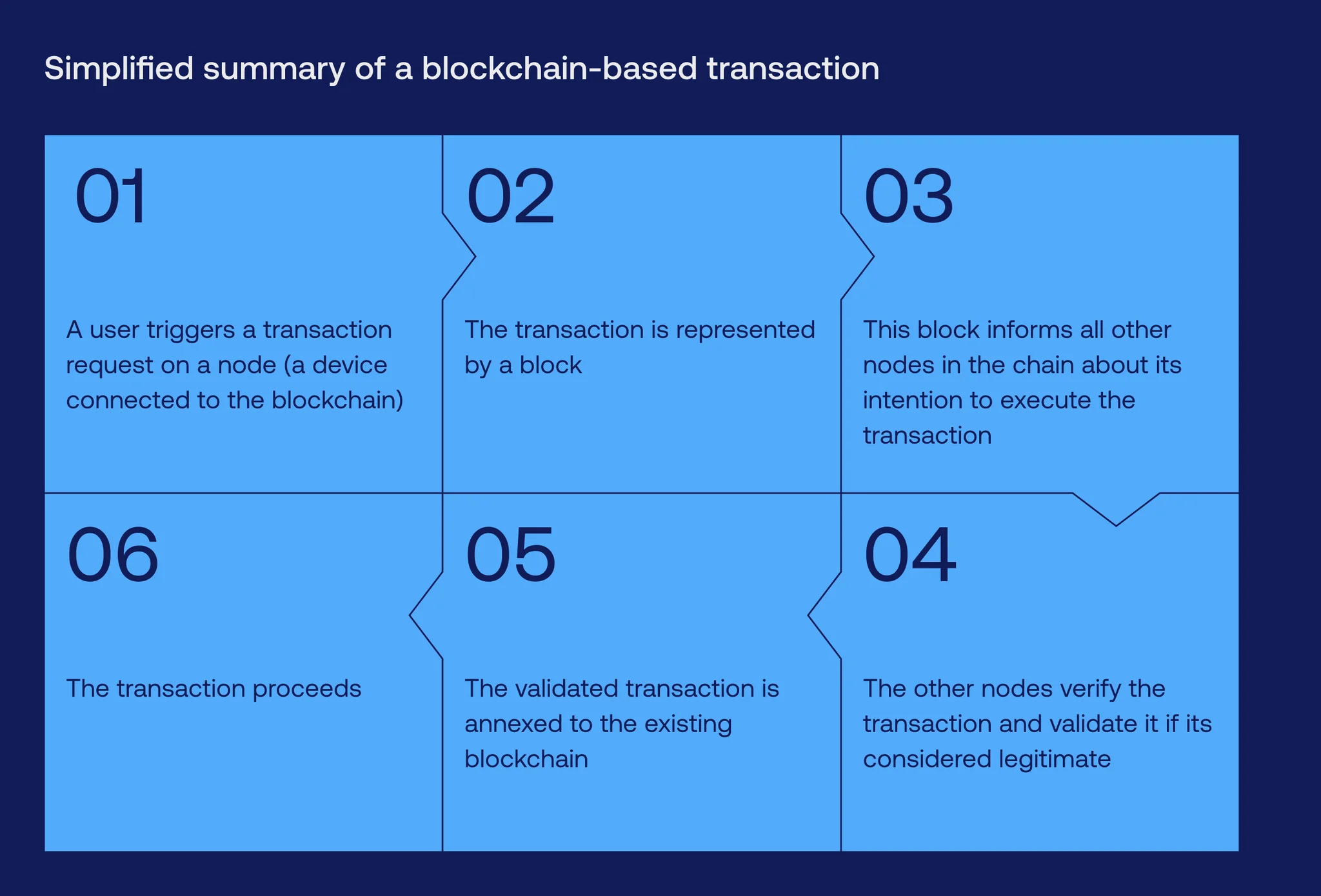

Blockchain for payments and its advantages

In a nutshell, blockchain allows transactions to be grouped into blocks and linked together in a chain, creating a tamper-resistant record. Now, apply blockchain for payments, and the result is a decentralized and secure ledger technology that can benefit both startups and enterprises by enhancing transparency, reducing costs, and mitigating fraud risks in corporate transactions — be it B2B or B2C.

For startups, blockchain offers a streamlined and cost-effective alternative to traditional payment systems. By eliminating intermediaries such as banks, startups can facilitate blockchain peer-to-peer payments and transactions without centralized oversight — basking in all those reduced transaction fees plus accelerated payment processing times. Additionally, startups can leverage smart contracts and self-executing agreements with predefined rules to automate payment workflows, saving time and resources.

On the enterprise level, blockchain provides a robust solution for large-scale financial transactions. It establishes a single, immutable ledger accessible to all participants, ensuring a consistent and auditable record whose transparency minimizes disputes and enables efficient reconciliation. Enterprises can also take advantage of the enhanced security features inherent in blockchain, guarding against fraudulent activities that threaten the integrity of their financial data.

Cryptocurrencies, often associated with blockchain, play a vital role in this ecosystem.

How can blockchain be used in payments?

For startups, accepting cryptocurrencies as payment can attract a broader customer base and facilitate international transactions without the complexities of traditional systems. On the other hand, enterprises can explore tokenization — representing assets or currencies on the blockchain — to optimize their payment processes further.

Both startups and enterprises can benefit from the decentralization of blockchain, which reduces reliance on a central authority and minimizes the risk of a single point of failure. This distributed nature enhances resilience and ensures continuous operation even in the face of disruptions.

Blockchain for payments: the market state for 2024

As a technology, blockchain already stands on its own merits in regard to market value. Revenue-wise, the global blockchain market is projected to generate over $94 billion by 2027, growing parabolic at 66.2% CAGR.

Surely, the biggest slice of that blockchain revenue pie is driven by the hundreds of cryptocurrencies that form the crypto market. In 2021, about 30 percent of blockchain’s entire market value in Europe was attributable to the banking sector, mostly due to how convenient the tech is for executing cross-border payments — a must for the continent’s multiple fiat currencies. And in 2022, 44 percent of global blockchain revenue derived from payments.

Source: Grand View Research

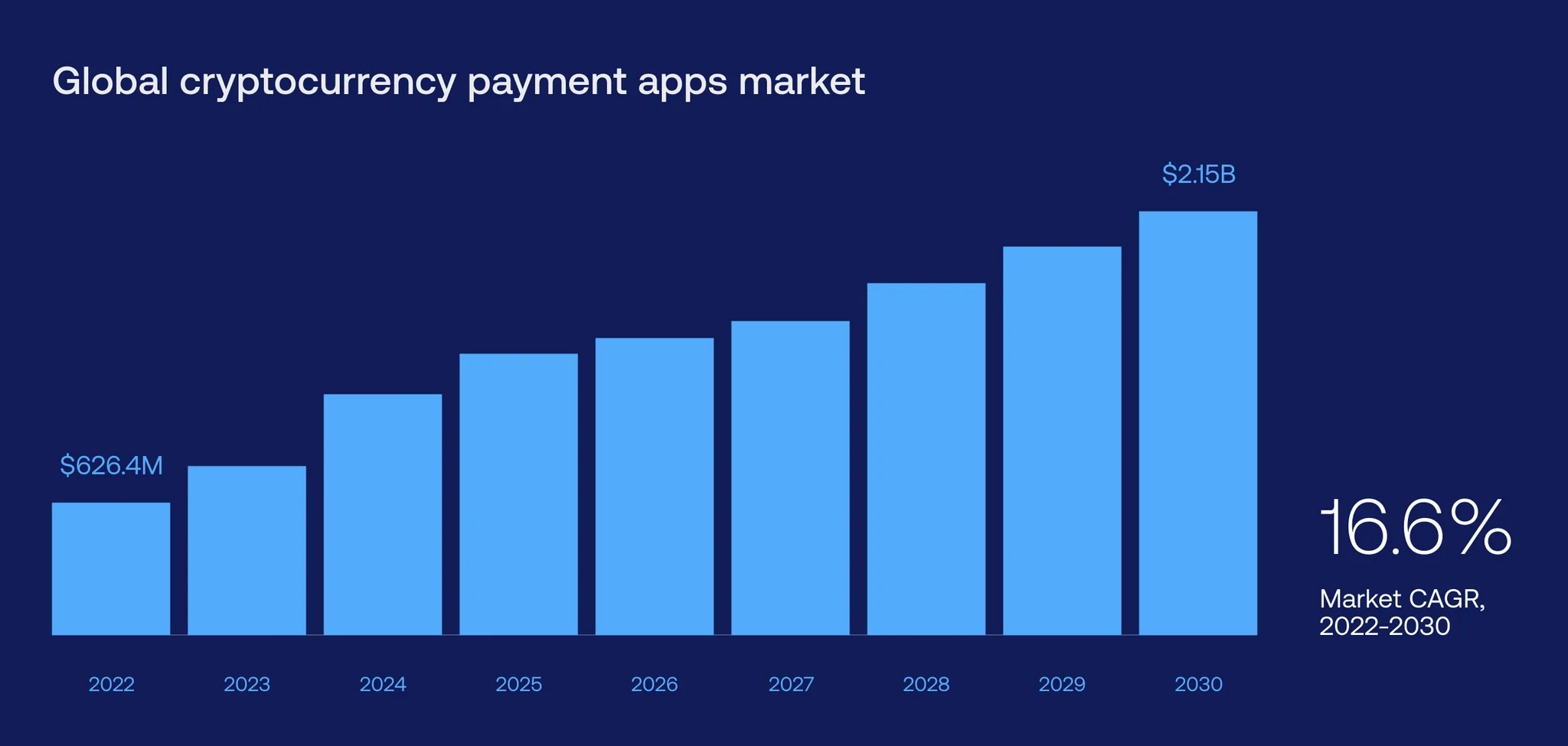

Meanwhile, has B2B joined the party yet? It sure did: Enterprises are poised to contribute over $4.4 trillion to the blockchain payments industry in B2B cross-border transactions worldwide by 2024. Hard to ignore the potential profits in the crypto payment market when it’s growing at 16.6 percent yearly, putting it on track to reach $2.1 billion by 2030.

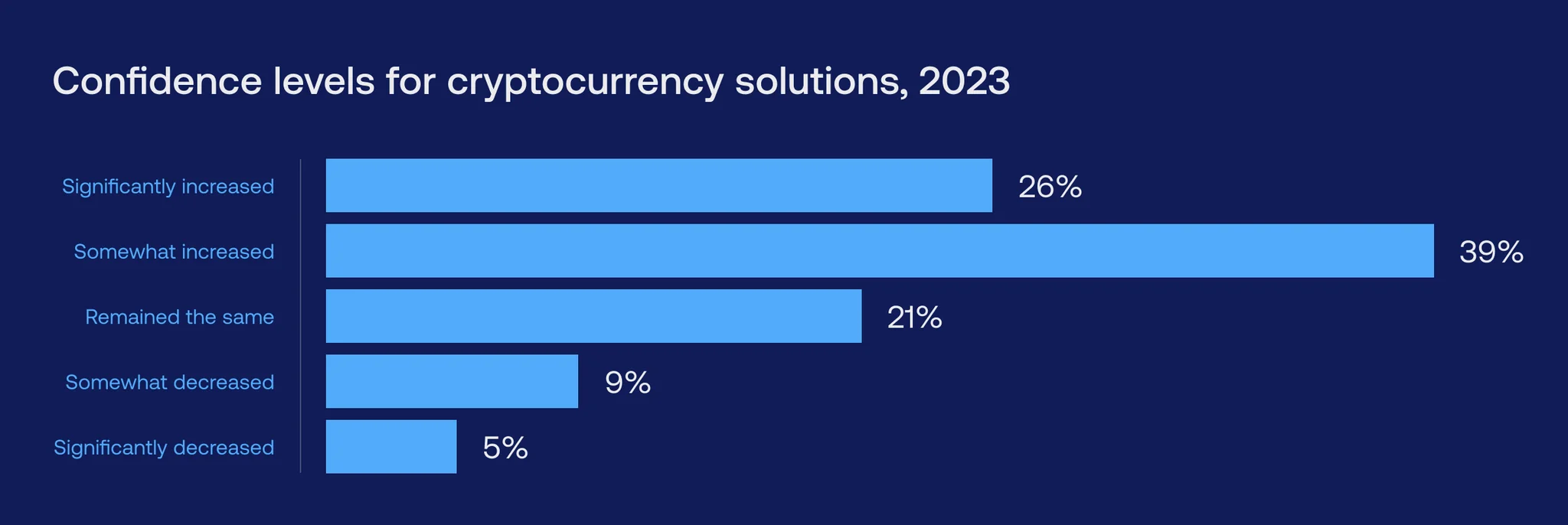

Most importantly, the confidence of global finance leaders in crypto has sharply increased in 2023. More than 90 percent believe that the currencies underpinned by blockchain will greatly impact business in the next few years. That naturally translates to a blockchain impact on payments.

That’s a lot of double-digit metrics for a piece of technology not called AI. But what exactly does blockchain software development bring to the payments table to be so enticing?

Traditional payments vs blockchain payments

It’s easier to consider the following characteristics not as oppositional, but complementary. Blockchain technology in fintech isn’t here to overtake traditional finance: It serves as a solid, legitimate financial alternative with its many pros and some cons to consider.

Authority – Centralized vs decentralized

-

Traditional payment systems, such as credit cards, bank transfers, or payment processors, rely on central authorities like banks and financial institutions to authorize and validate transactions.

-

Blockchain payments operate on a decentralized network of computers called nodes, which can verify transactions with node members without relying on a middleman.

Transactions – Intermediary vs direct

-

Traditional transactions often involve multiple intermediaries, each adding processing time and fees to the operation.

-

In blockchain transactions, participants can interact directly with each other without any intermediaries.

Privacy – Open vs closed

-

While traditional systems prioritize user privacy, they also require disclosing personal information to multiple third parties to enable transactions and meet regulatory requirements.

-

Blockchain transactions are pseudonymous, providing a degree of privacy while still keeping the transaction history transparent and verifiable to all participants.

Speed – Variable vs instant

-

Settlement times for traditional payments can vary from instant (depending on the region and financial institution) to quite lengthy, taking multiple days in the case of international transactions.

-

Blockchain international payments, especially those using stablecoins, can settle in real time or within minutes, providing unparalleled transaction processing.

Reversibility – Yes vs no

-

Traditional transactions are reversible, and disputes can be mediated through chargebacks or refunds according to the financial institution’s policies.

-

Blockchain transactions, once added to the chain, are irreversible and depend on legal action to be contested.

|

Purpose |

Traditional payments |

Blockchain payments |

|

|

Frontend |

Interaction with end-user (untouched by blockchain technology) |

Remains the same |

|

|

Messaging |

Technical connectivity with the network |

Through central infrastructure |

Direct peer-to-peer |

|

Processing |

Execution of transactions |

|

|

|

Ledger |

Keeps track of participants’ balances |

|

|

How blockchain improves payments

Now, where blockchain improves digital payments technology, it really does improve. It’s hard to argue against the underlying set of benefits that made blockchain take the financial world by storm: When implemented and used properly, its results are tangible to every single stakeholder.

Immutable record

Once a transaction is added to the blockchain, it becomes a permanent and unchangeable part of the ledger. This immutability enhances trust in the payment system, as participants can rely on the accuracy and permanence of the transaction history.

-

Trust – Any transaction data committed to the chain can’t be amended

-

Auditability – Auditors can quickly verify transactions by examining the chain

-

Accountability – The ledger’s unalterable record ensures all parties involved can be held accountable

-

Fraud prevention – Ledger tampering is trivial to detect, curbing out fraud attempts

Transparency

The blockchain ledger is transparent and accessible to all participants in the network. Each participant has a copy of the entire blockchain, reducing the risk of discrepancies or fraudulent activities as they can independently verify transactions.

- Public ledger – Ledger data is visible (though never editable) to all participants

-

Visibility of transaction details – Each transaction contains detailed metadata information

-

Autonomous verification – Transactions are validated by consensus before getting recorded in the chain

-

Real-time tracking – Network participants can monitor the movement of funds instantly for greater visibility

Reduced intermediaries and costs

Blockchain in digital payments can be used to streamline the payment process. It reduces the number of intermediaries involved, which speeds up the transaction process and further shrinks costs associated with third-party services.

- Decentralization – No need for a central authority to oversee operations

-

Peer-to-peer transactions – Blockchain eschews the middleman and lets participants trade directly

-

Smart contracts – The automated execution of agreements further removes the need for intermediaries

-

Reduced settlement times – Blockchain’s agility and lack of intermediaries minimize settlement times

Security

Blockchain uses cryptographic techniques to secure transactions. Each transaction is recorded in a block, and once the block is added to the chain, it becomes nearly impossible to alter, ensuring the integrity of the transaction history.

- Tamper resistance – All participants in the chain have a copy of the same ledger at all times to curb fraud by collusion

-

Access permission – Private blockchains count on a robust system of security clearances to ensure proper access permission

-

Secure hash functions – Each block in the chain is uniquely identified in a way designed to prevent their alteration without detection

-

Network resilience – Even if some nodes in the network become compromised, the remaining can operate independently to maintain integrity

Need a bit of guidance with blockchain payments technology?

Vention’s blockchain specialists have first-hand expertise.

Unexpected blockchain applications in payments

Blockchain is far from being a one-trick pony. Beyond the peer-to-peer transactions that made cryptocurrencies famous, blockchain technology in payments can be used for numerous purposes due to the versatility of a blockchain tech stack.

Supply chain payments

In the supply chain domain, blockchain enables the automation of payment processes as goods move through the chain, ensuring transparency and precise payment reconciliation. For instance, Walmart, after experimenting with provenance tracking of its pork products in China, now requires all its spinach and lettuce suppliers to deploy the technology.

Micropayments

Blockchain enables micropayments, or, in other words, transactions involving minimal amounts of money. This can underpin business models that rely on small but steady contributions from consumers. Content creators, for example, can benefit as consumers pay small amounts for access to digital content, articles, and other online services.

Point of sale (PoS) payments

Blockchain-based payment solutions can be integrated into point-of-sale systems, allowing merchants to accept cryptocurrency payments directly from customers. GoCrypto, a leading crypto payment provider, offers merchants various PoS solutions, such as all-in-one devices and apps that enable merchants to accept bank cards, digital payments, and cryptocurrencies — blockchain-based banking payments included.

Remittances and p2p blockchain payments

Blockchain can streamline the process of remittances by providing a more direct and cost-effective means of transferring funds internationally. Users can send and receive remittances without the need for traditional money transfer services, which often charge a premium for both currency conversion and international remittances.

Decentralized finance (DeFi)

DeFi platforms leverage blockchain to offer decentralized financial services, including lending, borrowing, and trading, so users can participate in financial activities without relying on traditional banks. Unlike legacy institutions, DeFi entities such as Maker (developers of DeFi app Oasis) accept cryptocurrency security on the platform, with straightforward systems to establish creditworthiness.

Digital identity and KYC

Blockchain improves Know Your Customer (KYC) processes by providing a secure and transparent way to manage digital identities. Users can store their ID data and credentials in a decentralized identity wallet app with the blockchain, allowing this data to be instantly verifiable without contacting the issuer. Beyond reducing the risk of identity theft, this also streamlines onboarding processes for financial services.

Charitable donations

Blockchain can enhance transparency and traceability in charitable donations. Donors can track how their contributions are utilized, ensuring accountability and reducing the risk of fraud. The World Food Program (WFP), for example, has incorporated cash transfers for humanitarian assistance; the company implemented blockchain technology to improve the efficiency and transparency of these transfers and currently empowers 4M+ people monthly.

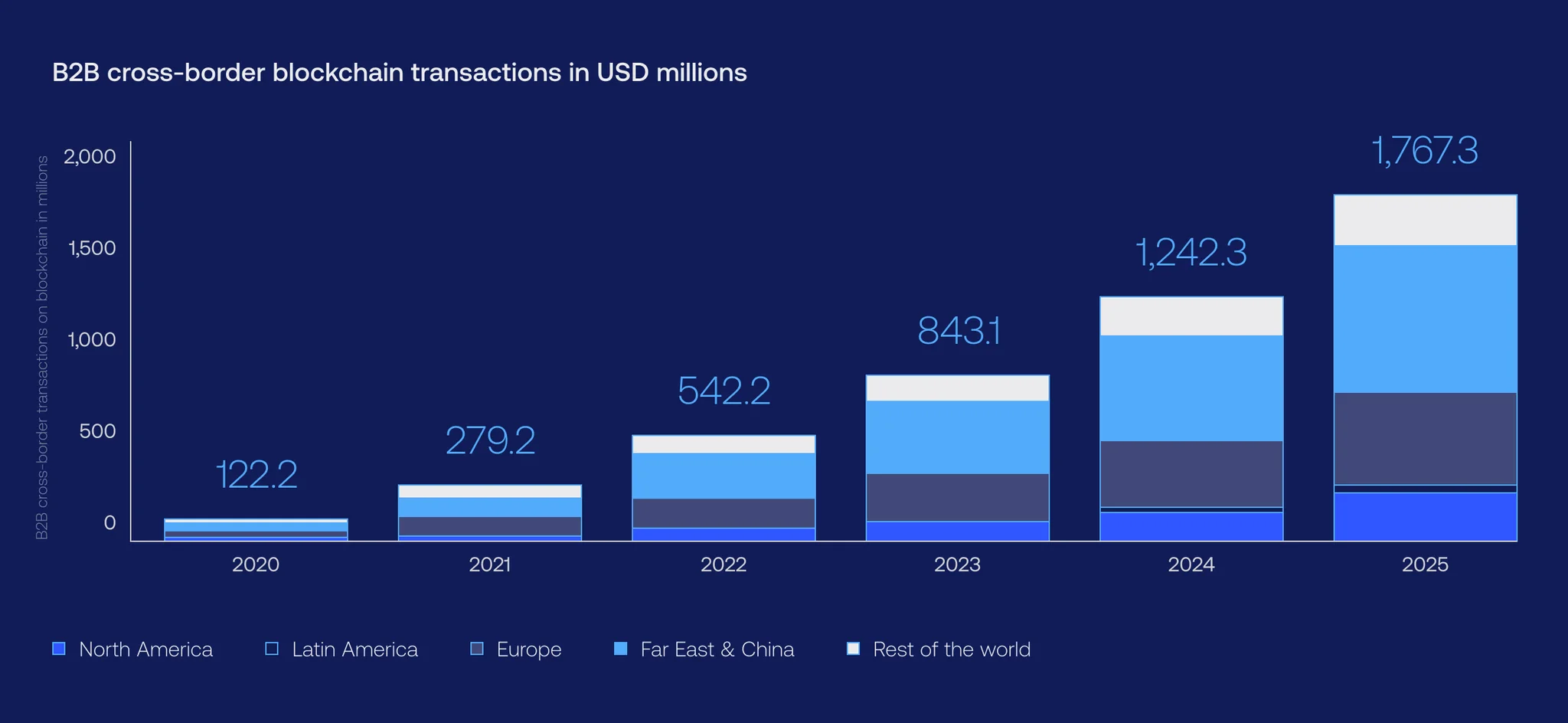

Blockchain in cross-border payments and how it works

Perhaps the tech’s greatest edge regarding transactions, blockchain for cross-border payments offers significant advantages for entrepreneurs looking to streamline international transactions. It allows for direct peer-to-peer transactions without the need for the usual intermediaries.

And the enterprise sector is taking note of this blockchain for B2B payments bonanza, with global B2B cross-border transactions on the blockchain projected to reach $1,7 billion by 2025. Other benefits include:

Source: Statista

Currency agnosticism

Blockchain is currency-agnostic, meaning it can facilitate transactions in various currencies. Operators can transact directly in digital currencies or use blockchain platforms that support multiple fiat currencies.

Payment platforms and services

Various blockchain payment platforms and services cater to cross-border transactions. Entrepreneurs should research and choose platforms that not only meet their specific business needs, but are also user-friendly, scalable, and secure.

Volatility management

Cryptocurrencies, in particular, are notorious for their price volatility. Strategies for managing it (such as using stablecoins linked to fiat currencies) may be employed to mitigate risks.

Integration with existing systems

Compatibility with legacy systems is paramount to guarantee seamless integration. Luckily, blockchain payments can integrate with most existing financial and accounting systems.

Network scalability

Entrepreneurs must consider the scalability of the chosen blockchain network to ensure it can handle increasing transaction volumes as the business grows.

Risk management

While blockchain offers enhanced security, decision-makers building a payments solution should conduct a thorough risk assessment that considers factors such as regulatory changes, market volatility, and technology risks.

Regulatory compliance

Entrepreneurs should be aware of regulatory considerations in different jurisdictions. Some regions have specific regulations governing cryptocurrency and blockchain transactions, and abiding by them is crucial for a smooth cross-border payment experience.

The regulatory landscape of blockchain payments

The regulatory treatment of cryptocurrencies, which often underpin decentralized payment systems, varies globally. Some countries have embraced and regulated cryptocurrencies, providing legal frameworks for their use. Others have imposed restrictions or outright bans.

Governments worldwide are concerned about the potential misuse of decentralized payment systems for illegal activities, such as money laundering and terrorist financing. The Fifth and Sixth Money Laundering Directives (AMLD 5, AMLD 6) in Europe and FinCEN’s Final Rule in the USA make it clear that virtual currencies and their trade exchanges are subject to anti-money laundering legislation (AML).

Therefore, regulations often include AML and KYC requirements for cryptocurrency exchanges and businesses involved in decentralized payments.

Securities and CBDCs

Decentralized projects may involve the issuance of tokens that, in some cases, could be classified as securities. Securities regulations may apply, and compliance with these regulations is necessary to avoid legal issues.

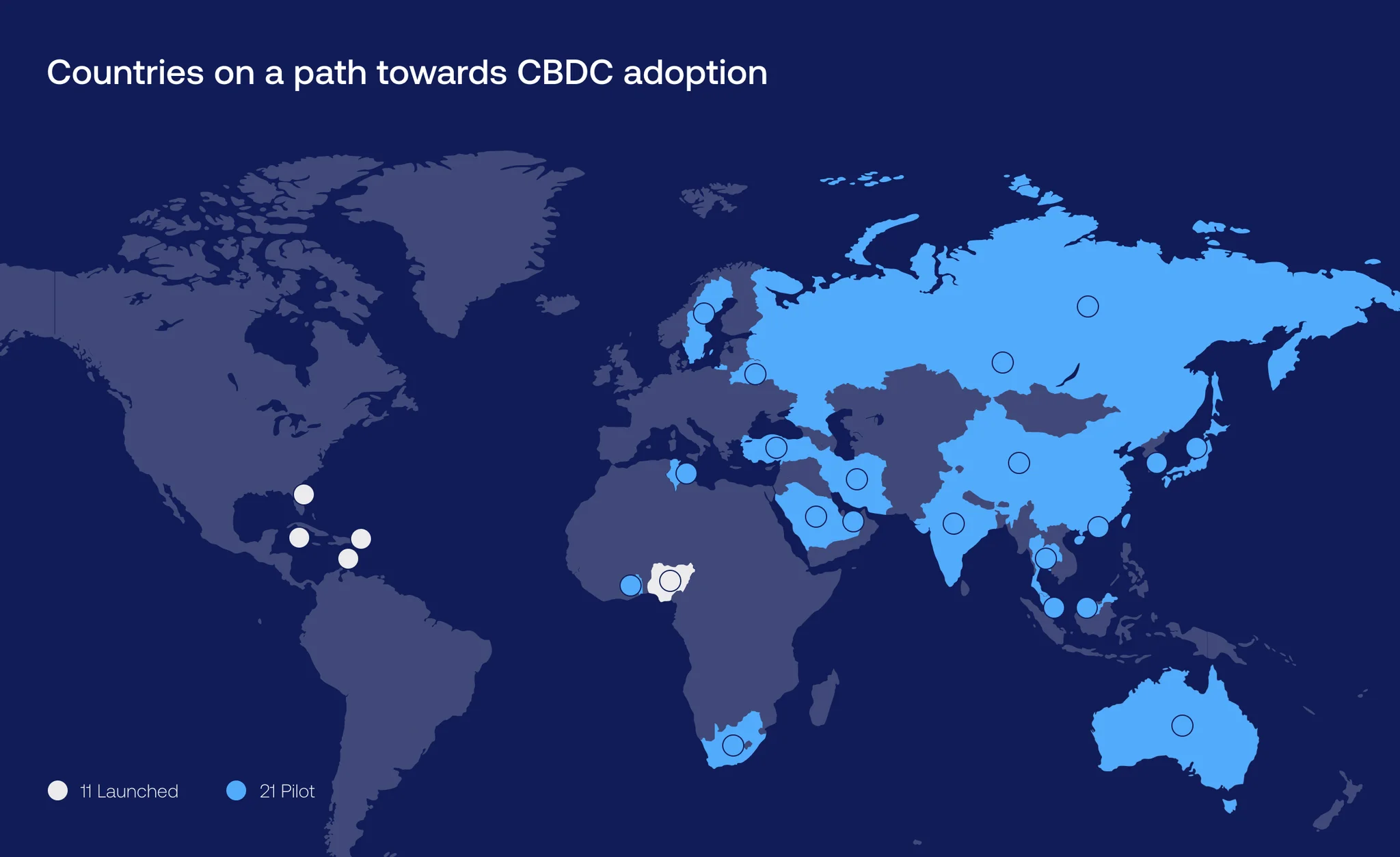

The development and potential issuance of central bank digital currencies (CBDC) by various countries add a layer of complexity to the regulatory landscape, as the relationship between decentralized cryptocurrencies and CBDCs may influence regulatory decisions.

To date, 11 countries have fully launched a digital currency. Furthermore, 19 of the G20 countries are now in the advanced stage of CBDC development. Of those, nine countries are already in the pilot. Nearly every G20 country has made significant progress and invested new resources in these projects over the past six months.

Source: Atlantic Council

Blockchain payments taxation

Tax treatment of decentralized payments and transactions involving cryptocurrencies can vary. Some jurisdictions tax cryptocurrencies as assets, while others treat them as currency.

Understanding the tax implications is crucial for businesses and individuals involved in decentralized payments. In the US, according to the IRS Notice 2014-21, businesses are taxable regardless of whether they receive cash or crypto as payment for goods and services since both cases generally fall under ordinary income. For tax purposes, crypto is considered property, so the income is measured by the fair market value of the crypto at the time of receipt.

Smart contracts

Legal recognition of smart contracts, integral to many decentralized payment systems, is an evolving aspect of blockchain regulation. Some jurisdictions have taken steps to recognize smart contracts as legally enforceable. In the US, The E-SIGN Act and UETA are federal laws that affirm the legality of electronic signatures and records.

Enacted in 2000 at the height of the e-commerce boom, the E-SIGN Act validates electronic signatures and records in interstate and foreign commerce, making electronically entered contracts legally binding. Similarly, UETA grants legal status to electronic records and signatures, treating them in the same measure as traditional paper documents.

Both Acts support the notion that smart contracts, operating on blockchain technology, should be considered legally enforceable, as electronic records and signatures cannot be denied legal status solely due to their electronic form.

Looking for regulatory advice in your blockchain project?

Our fintech experts are free for a consultation.

Decentralized payments and their legal status

Some countries have introduced regulatory sandboxes that allow businesses to test new technologies in a controlled environment, including decentralized payment solutions. Beyond encouraging innovation, this helps regulators understand the technology's implications.

In the US, the Consumer Financial Protection Bureau (CFPB) was the first regulatory agency to set up a dedicated fintech office to provide assistance to promote innovation. The CFPB has policies — such as the No Action Letter (NAL) policy — that perform many of the functions of a sandbox. At the state level, Arizona, Wyoming, and Utah have launched sandboxes, and other states are at various stages of exploration.

In Canada, the Canadian Securities Administrators (CSA) has launched a regulatory sandbox for fintech and other innovative companies. Firms with innovative business models are invited to contact their local securities regulator to discuss the firm’s business model and applicable securities law issues.

Across the Atlantic, the European Regulatory Sandbox for Blockchain provides legal certainty for decentralized solutions by identifying obstacles to deployment from a regulatory perspective — through legal advice, regulatory experience, and guidance in a safe and confidential environment. Scheduled to run until 2026, the Sandbox supports 20 projects annually, including public sector use cases on the European Blockchain Services Infrastructure (EBSI), a project involving multiple EU member states.

In the UK, the FCA Regulatory Sandbox offers innovators (both established and new) access to regulatory guidance across all financial services sectors. It allows firms to test products and services in a controlled environment, providing insights into consumer appeal and market dynamics. Participants benefit from a faster time-to-market at potentially lower costs and receive support in identifying and implementing consumer protection measures for new offerings, which is key to turning the blockchain consumer payments market into a robust, matured environment.

Other regions worldwide offering sandboxes for high-tech startups and enterprises include Singapore, Australia, the UAE, Malaysia, Bahrain, Hong Kong, and Saudi Arabia.

Blockchain payments: regulatory trends for 2024

Albeit timidly, governments worldwide have been on a steady path to recognize cryptocurrencies (and, thus, blockchain-based payments) as a reality. Reality as in legal tender. Back in 2021, El Salvador was the first country to adopt Bitcoin as an official currency. In Europe, the Swiss canton of Zug — aptly nicknamed “Crypto Valley” — has already normalized accepting tax payments in crypto.

As Ivan Pilnikau, Vention’s blockchain specialist, explains, "Some blockchain advocates see a battle between the traditional finance system and decentralized ones right now, but hybrid systems have already won. It’s just a matter of time until more and more governments realize that fiat and crypto can, should, and will coexist peacefully.”

Here’s how some of the world’s biggest markets are deploying their regulatory infrastructure regarding blockchain-based payments:

United States

The US Internal Revenue Service presented proposed section 6045 regulations, which aim to bring clarity and alignment to tax reporting rules for brokers handling digital assets, ensuring that they adhere to the same information reporting standards as brokers dealing with securities and other financial instruments.

Under the proposed rules, 2026 will be the first year when brokers are required to report any information on sales and exchanges of digital assets.

Canada

In Canada, when virtual currency is used for salary or wages, it is generally considered part of the employee's income in Canadian dollars. Virtual currencies, classified as commodities, follow barter transaction rules when used to buy goods or services.

Consequently, the income for tax purposes is based on the Canadian dollar value of the purchased goods or services, not the virtual currency value. However, the Canada Revenue Agency (CRA) specifies that the fair market value of the virtual currency at the time of the transaction should be used to calculate goods and services tax (GST) and harmonized sales tax (HST) for taxable supplies.

European Union

The Council presidency and the European Parliament have reached a provisional agreement on the markets in crypto-assets (MiCA) proposal, encompassing regulations for unbacked crypto-assets, stablecoins, trading venues, and crypto-asset wallets. The new rules mandate crypto-asset service providers to adhere to stringent requirements to safeguard consumer wallets, holding them liable for any loss of investors' crypto-assets.

Providers with parent companies in high-risk countries for anti-money laundering or non-cooperative jurisdictions for tax purposes must implement enhanced checks aligned with the EU AML framework. National authorities are required to issue authorizations within a three-month timeframe — and by December 2024, the European Commission will assess the need for a specific legislative proposal addressing non-fungible tokens (NFTs) and emerging risks in this market.

United Kingdom

The UK, aspiring to establish itself as a global cryptocurrency hub, successfully incorporated stablecoins into the country's payments regulation in June 2023. Legislation specifically for fiat-backed stablecoins is anticipated for early 2024.

Both the Financial Conduct Authority (FCA) and the central bank plan to release final rules through consultations by mid-2024, with the stablecoin regulatory framework set to be implemented by 2025. The FCA emphasizes that issuers must obtain authorization to circulate fiat-backed stablecoins in or from the UK, meaning that stablecoins must be backed by suitable assets equivalent to their circulating value and also be easily redeemed for fiat currencies despite technical or liquidity challenges.

Still uncertain about blockchain?

Get our expert guidance for your blockchain initiative.